Dallas Foreclosures in Steady Decline

Home buyers and sellers alike can rejoice in the fact that the real estate market continues to improve. Gone are the days of the housing market crash where properties and homes were extremely difficult to sell and foreclosure rates were at an all-time high. Home and property foreclosure rates have been steadily declining over the past couple of years, and the Texas area is one of the areas where a decrease has been extremely significant. According to bizjournals.com, the Dallas, Texas area has been seeing a steady decrease in foreclosure figures since January of 2013.

The number of foreclosures in the Dallas area was found to be significantly below the foreclosure rates for the nation, according to statistics gathered by Irvine, California-based CoreLogic. The Dallas-Plano-Irving area’s foreclosure rates were found to have declined to 1.25 percent, a decrease of 0.31 percentage points in the month of January alone.

Overall, the North Texas area saw a foreclosure rate of 1.17 percent in January, a figure significantly lower than what was found for the national foreclosure rate which was 2.90 in January, according to bizjournals.com. Additionally, the Texas area has also seen a decrease in the mortgage delinquency rate with rates decreasing from 5.16 percent to 4.28 percent in January. Delinquency rates are usually determined by factoring in mortgage loans that are past due by 90 days or more. The lowered foreclosure rates and delinquent mortgage rates is a great sign for the Texas area housing market.

If you are interested in learning more information about loan opportunities in Dallas and its surrounding areas, please give us a call. We’d be delighted to share all the mortgage options that might help you in your quest to find a home.

Dallas Housing Construction Increases as Mortgage Rates Drop

Home construction is on the rise in North Texas, according to a report from star-telegram.com. Construction on new homes has reached a 5-year high, as more people relocate to the Dallas area.

Low rates on Dallas mortgages are playing a big role in the new housing construction, according to Ted Wilson, principal with Dallas-based Residential Strategies. Thirty-year fixed mortgage rates recently hit near-historic lows, and Wilson sees both low mortgage rates and a general economic upturn as reasons why people are buying more new homes in Dallas.

Job growth is another factor that has influenced increased housing construction. MetroStudy’s Dallas-Fort Worth regional Director David Brown said, “It is likely home builders will start over 20,000 homes in 2013.” Home construction was up 35% for the first three months of 2013, compared to the same three-month period in 2012, with 4,312 new homes built in North Texas.

Compared to 5 years ago, there are also far fewer vacant homes in the Dallas Forth-Worth area. While a similar number of homes were constructed in 2008, there were more than 6,000 vacant homes at the end of March of that year compared to only 3,182 vacant homes at the end of March, 2013. This data further suggests a burgeoning housing market.

There are many great homes for sale in the Dallas area, and we would love to help you find the loan program that is right for you. For more information about Dallas mortgages, please contact us.

What’s Your Rate? Home Loan Rates Spike with Stocks at All-time Highs

Home loan rates determine how much you can afford, how much you can qualify for, and much more. That’s why one of the first questions people ask when they talk to a lender, Bank or mortgage company is ‘What’s your rate?’…and for good reason.

What’s your rate?

There’s no single answer to the question. There are many factors that have to be taken into consideration to determine an interest rate. Credit score, Down payment, Loan amount, Loan term, Fixed/adjustable, Market movement etc…

While many of the variables to determine a rate may already be known, the market movement causes interest rates to fluctuate up/down each and every day.

So, what’s YOUR rate? If you thought you knew, it may have changed more than you think, so here are a few tips when interest rates are moving:

- Has your rate changed? Ask your lender to provide an updated rate quote based on the current market.

- Where are rates headed and should you lock before they get worse? Find out the recommendation and opinion on when to lock in your interest rate. It’s your call but you should be able to rely on the advice and opinion of your lender to make a decision. If you don’t, find someone who can provide up-to-date interest rate and market information.

- Are you pre-approved? If so, should you be ‘re-approved’? When rates are rising, there is no certainty behind how much they can increase and how much your payment can increase. Could interest rates go up so much that you could no longer qualify for the payment? Pre-approval and ‘Re-approval’ can help you:

- Be in a position to make an offer immediately

- Lock in your interest rate, before they go up, as soon as you find a home

- Close fast! In a seller’s market – closing fast may be the difference in your offer being accepted

Rates Are Still Low…But Stocks are Forcing Rates Higher

There’s no question that interest rates are still extremely low and not too far away from being at historically low rates. That is one amazing opportunity that can help people afford more house than they ever have in the past. But how much do home loan rates have to rise before it starts to impact the house you are trying to buy?The stock market continues to rally and set all-time highs. I’m happy to hear that and hope people are making some money. The downside of that is that stocks have climbed to record highs at the expense of home loan rates. If that person is looking to buy a house or refinance, they may need that extra money to make up for the spike in interest rates over the last week.

Home loan rates have increased in large part due to the rally in the stock market. Why? Because lots of the people buying stocks right now had been sitting on the sidelines holding onto their cash, making minimal returns holding things like mortgage backed securities. Opportunity arises to make more money in the stock market? Adios! I’m selling these low rate mortgage backed securities and making money in stocks — the end result is stocks go up and so do home loan rates.

Lowest Jobless Rate in Four Years Drives Rates Higher

Compounding with the rising stock market, and helping fuel it and home loan rates higher for that matter, was a report of the lowest jobless rate in four years. Once again, another signal to global markets of a growing economy and job force.

While stocks continue to rally and the economy shows signs of expansion, home loan rates are going to continue to go up and increase the cost for homeowners to buy homes. But you were prepared for this, right?

If you or someone you know have been in the market to buy a house. First, make sure they are pre-approved. Second, encourage them to ask or re-ask the question, ‘What’s your rate?‘ and make sure they are still comfortable with not only their rate, but with their lender as their guide.

If our team can be a resource, always feel free to call and talk to a real person at 972-499-0454.

Home Loan Rates Jump on Hopes of Rebounding Economy

Home loan rates jumped higher over the last week as hopes of a rebounding economy start to appear on the horizon. The rosy economic outlook has helped the stock market rally to its highest levels in 5 years has force home loan rates and mortgage bonds to see their worst levels in recent months.

Rebounding Economy = Rebounding Home Loan Rates and Home Prices

A rebounding economy isn’t great news for everyone. Prospective home buyers have started to see their potential monthly mortgage payments increase. Home loan rates have jumped from as much as .25 – .375%, raising monthly payment costs by close to 10% in some cases. As the economy starts to establish a footing to rebound and grow, expect home loan rates, home prices, and home payments to increase as well.

The rebound in the economy could be a false alarm, only time will tell. In the mean time, the hopes and rally behind a growing economy are based off some recent reports.

- Strengthening Job Market – Lowest initial jobless claims in 5 years

- Brightened global economic outlook based on Germany’s increasing growth

- Stocks rally to 5 year highs

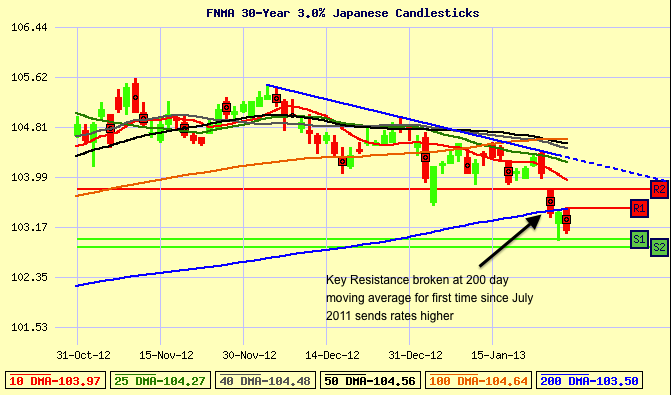

Stocks Rally and Home Loan Rates Suffer

Home loan rates have been rising as investors shift their money out of Bonds and treasuries to the stock market. Currently the stock market is at the best level in years, but mortgage bonds have suffered and broken through key resistance at the 200 day moving average. The breakdown of this technical level coupled with the rising stock market have driven mortgage bonds drastically lower, providing a reminder of how quickly home loan rates can rise.

Home loan rates have been rising as investors shift their money out of Bonds and treasuries to the stock market. Currently the stock market is at the best level in years, but mortgage bonds have suffered and broken through key resistance at the 200 day moving average. The breakdown of this technical level coupled with the rising stock market have driven mortgage bonds drastically lower, providing a reminder of how quickly home loan rates can rise.

Time Is Running Out for Historic Home Affordability

Despite a recent uptick in home loan rates and home values, owning a home in Dallas and around the country is more affordable than ever. If you or a someone you know has goals to own to pursue your dream home by creating a plan. Find out what you can afford. We are happy to be a resource and invite you to complete a Home Purchase Review to help guide you in the right direction.

Will Raising the Debt Ceiling Raise Home Loan Rates?

Congress has found itself in another sticky situation that could raise home loan rates. Less than a month since the country was teetering on the edge of the ‘fiscal cliff,’ Congress now needs to raise the ‘debt ceiling’ beyond its current limit of $16.4 Trillion to avoid default on debt. The question on the minds of homeowners and home buyers is “Will raising the debt ceiling raise home loan rates and cost me more money in the long run?”

Despite the looming crisis over the debt ceiling, home loan rates continue to sit near historic lows, allowing families in Dallas and across the country to save money by refinancing or buying a new home. Apparently Congress has a little bit of a spending problem. The Congressional budget is set higher than the projected revenues nearly every year, leading to frequent debt ceiling increases. In fact, the debt ceiling has been raised 76 times since 1962, 11 of which have occurred since 2001.

Typically an increase to the debt ceiling is just another day in the office for Congress. A revised debt ceiling is proposed, approved by Congress and the President, thus allowing Congressional spending to continue as usual. However, when the House and Senate don’t agree on the current spending plan or increase of the debt ceiling, talk and fear of consequences begin to emerge.

What happens if the debt ceiling is not raised?

Failing to raise the debt ceiling would have many possible consequences. Essentially, Congress will run out of money at some point during the year and the Treasury will be responsible for deciding on which things to include in the budget:

- Elimination of military benefits

- Limitation of social security payments

- Failure to pay government contractors and agencies

- Default on national debt by not repaying bond holders

When weighing these options during a similar debt ceiling crisis in 2011, Fed Chief Ben Bernanke said “The United States would be forced into a position of defaulting on its debt. And the implications of that for our financial system, for our fiscal policy, for our economy would be catastrophic.”

A default on national debt would carry the greatest impact on costs for homeowners and prospective home buyers. For centuries the U.S. has been borrowing money from investors through sale of bonds, promising a dependable repayment and return. Any increased risk default on this type of national debt is likely to raise concerns and costs for the U.S. to borrow money.

Higher Risk Leads to Higher Rates

Whether a home loan, auto loan or credit card, when applying for credit, the creditor will be asking the question, “How much risk is there to receive repayment on the loan?” The higher the risk of repayment, the higher the interest rate to borrow the money. Investors in Bonds are no different. The more risky they feel it is to get their money back, the more interest they’re going to charge.

The U.S. is fortunate to issue what is considered a very low-risk bond. A safe haven for investors to park their funds despite a low rate of return. In recent years, countries like Greece, Italy, Ireland, Portugal and Spain also issued what was considered a “low-risk” bond.

That was until the countries spending problems and economic woes showed real signs of risk and default on their national debts. For investors and bond holders, the once “low-risk” investment was in jeopardy of default and no longer worth the low rate of return. The increased risk resulted in a fire sale of the bonds and a huge increase in interest rates and costs for those countries to borrow money.

Safe haven for borrowing money but how safe?

With the U.S. Congress facing further debate to raise the debt ceiling and avoid default on national debt, the path going forward looks eerily similar to those once “low-risk” bonds of Greece, Spain, etc. Issues like the ‘fiscal cliff’ and ‘debt ceiling’ continue to show how out of control spending can increase the risk of bonds and could likely lead to higher rates for bonds and even home loan rates.

A homeowner on the fence about refinancing, a current owner planning to sell a home and buy a new one, or a renter planning to buy a first home are each in a position to save lots of money at today’s current low rates. Waiting too much longer is likely to lead to higher costs and home loan rates. It’s time to create a plan of action and start taking the first steps or at least start becoming familiar with the process. We are happy to be a resource regardless of the stage in the process.

Mortgage Rates Rise After Fed Hints at End to QE3 In 2013

Home loan rates moved up to their worst levels since mid-August after the Fed hints at stopping the QE3 purchase program by the end of 2013. The QE3 purchase program currently allows the Fed to purchase $40 billion per month in an effort to keep rates low. While many Fed members still feel that the QE3 bond buying is a necessary evil, others feel that accumulating another $1 trillion over the next year (yes, Trillion, with a T) may not be warranted since the economy is showing signs of improvement. After release of the news, mortgage rates were crushed, causing home loan rates to increase by nearly .25% in less than 24 hours.

How Does an End to Quantitative Easing (QE3) Affect Mortgage Interest Rates?

While the QE spending has likely helped keep interest rates at or near historic lows, the Fed comments about ending QE3 quickly provided a glimpse into how much the Fed’s purchase programs are influencing the market. The Fed released minutes of their FOMC meeting and hinted at an end to the QE3 Bond buying at some point in 2013. The markets immediately took this as a sign that interest rates should be higher since the Fed would no longer be purchasing $40 Billion per month in securities that would artificially sustain low rates for home buyers. Without the Fed providing the massive purchasing power of Mortgage Backed Securities to keep rates low, a normalcy will come back to the market, leaving interest rates at a higher, more sustainable level.

- Higher mortgage interest rates – Fed will no longer be purchasing bonds to keep prices high and rates/yields low

- Lowers liquidity in the markets – less money printed and available to purchase bonds = less bond buying overall

- Increase in volatility – Mortgage rates more likely to be affected by global and U.S. economic reports

QE3 is old news – Will QE4 Help Keep Interest Rates Low?

QE4 was announced in early December ’12 as another monetary stimulus package. The QE4 purchase program is very similar to QE1, 2, and 3 as an attempt to stimulate the economy through a targeted Bond buying program. The QE4 plan adds an additional $45 Billion in Bond purchases to the $40 billion already in place from QE3. The difference is the Bonds that are targeted by each QE stimulus package.

- QE3 is aimed to target the purchase of $40 Billion in Mortgage Backed Securities (the bonds that directly influence home mortgage rates)

- QE4 on the other hand is aimed at the purchase of $45 Billion in long term treasury notes

While QE4 will help keep long-term Bond prices and yields low, QE4 does not directly impact home mortgage rates.

Where are Interest Rates Headed Moving Forward?

The Fed views a recovery in the real estate market as one of the greatest opportunities to turn-around the economy. An increase in real estate volume and home prices would not only help people who have spent the last 10 years underwater (owing more than the home is worth), but also stimulates the many industries that benefit from real estate growth and expansion. The mortgage lenders, title companies, general contractors, home builders, home warranty companies, etc… all stand to benefit from a boost in the real estate markets. The Fed understands this and will continue to artificially influence home loan rates to make sure the real estate markets can continue to grow. However, people don’t buy houses, they buy payments. Rates alone do not drive someone to purchase a home, rather the price range that they’re looking to purchase a home.

In the next 12 months we do expect home loan rates to increase to a more “normal” and sustainable level. While interest rates aren’t expected to jump to 6% overnight, part of a real estate recovery will be paced with a steady increase in rates. The announcement of a potential end to QE3 in the calendar year may be the tip of the iceberg towards a trend of higher interest rates in months/years to come.

Get Ahead of the Mortgage Curve When Purchasing Your Dallas Home

All signs are pointing to a rebounding real estate market in 2013, data from the National Association of Realtors suggests. Median home prices continue to rise yet still remain below their 2007 highs, suggesting a real estate “sweet spot.” The new year will usher in more choices and the Dallas area has been specifically cited by a chief economist expert at Zillow as a region with major finds waiting to be discovered

Despite upticks in supply and demand, mortgage rates are running at unprecedented values and in fact, continue to dip. According to The Wall Street Journal, in mid-November, the 30-year fixed-rate dropped below 3.5%, while the 15-year mortgage remained under 3%. And, the Federal Government has been consistently transparent about maintaining interest rates at such attractive costs for the next 30 months, at a minimum.

But if real estate has proven anything, it is its own unpredictability. A sudden surge of new buyers and sellers could conceivably bring rate changes in the Dallas mortgage market but at the very least the influx might slow down application processing. Our suggestion is to lock up your mortgage position before the rush, especially with Dallas being called out as having some of the most attractive real estate opportunities in the country.

We can help you lock in these historic rates now and avoid the anxiety of watching your dream home be purchased by another owner ahead of you in the mortgage curve. Please contact us for more information about Dallas real estate and mortgage options.

Mortgage Rate and Real Estate Update – Week of 12/17/12

Tired of hearing about the fiscal cliff and quantitative easing (QE)? Me too. However, there are some key things on the table in Congress that may affect the house that you own or are thinking about buying.

- Is now the time to sell your home in the Dallas-Fort Worth area?

- Blogs writing blues got you down? Find out how to be a curator of content and have a surplus of topics for the New year

- Zig Ziglar – Life lessons from a ‘big brother’ and mentor

Fiscal Cliff and the Impact on Mortgage Rates and Deductions

Another week has passed without resolution to the ‘fiscal cliff’ that is ahead of us. In short, the ‘fiscal cliff’, a term coined by Fed Chief Bernanke, describes a massive shortfall in revenues (taxes) in comparison to the budget. Last year, Congress spent $3.6 trillion and only brought in $2.3 trillion in revenue, a shortfall of over 56%. If a family were to budget their finances in the same manner, they may have earned $100k in income for the year but ended up spending every dime they earned, saved zero dollars and would have racked up over $56,000 in additional credit card debt. No bueno, especially when the spending has been that way for years and years. Sorry U.S. government, no home loan for you!

So with a $1.3 trillion shortfall going forward, cuts must be made to the budget and tax revenues must be increased. Easy targets could be things like Homeland security, Energy or the Interior budget (No, not home furnishing for the White House), but these items are so small and would only account for less than 2.5% of the overall budget. The cuts will have to come from bigger components, things like Social Security, Health and Human Services, or Defense, each of which is held close to the heart of one of the powers in Congress, whether the Defense for the GOP or social programs for the Dems. Therein lies the stalemate so far. Two ways of thought and two ways of spending that must reach a common ground.

However, regardless of where the cuts come from, the Tax revenues will have to be increased. One sure way will be to raise taxes for those considered to be the ‘wealthiest Americans’, but the definition of those ‘wealthiest Americans’ is vastly different between party lines. Republicans have acknowledged these Americans to be earning $1 million and higher where the President stands behind his definition as those earning upwards of $250k. Whatever the collective definition ends up becoming, there will be additional tax revenue to help reduce the shortfall.

Aside from tax hikes for the wealthy, additional revenues will likely come from the elimination of certain tax deductions. The one near and dear to our hearts is the mortgage interest tax deduction, which currently allows owners of a primary residence to deduct the interest that they pay each year from their overall income, thus reducing their tax liability. Millions of American families are able to apply this deduction to their taxes each year and save on average $5,459 on their tax bill. Will this cause a slowdown for housing as home buyers see less incentive to buy instead of rent?

Other tax deduction caps are likely to come into the fold, possibly placing a cap on the total deductions that someone can take. For most individuals, the caps will be a non-issue, but for self-employed and small business owners, the caps will change the way their businesses and accounting practices are structured.

The Fed Introduces More Easing to Keep Rates Low

Amidst the talks of the fiscal cliff, the Fed held is closed-door meetings last week and announced its Fed Policy Change on Wednesday 12/12/12. Fed Chairman Bernanke announced that the Fed will begin spending an additional $45 billion per month, targeting longer term Treasury securities, replacing ‘Operation Twist’ which expires at year-end. The big twist came when the Fed decided to no longer use a specific timetable to indicate an end to the monetary policy. Instead the Fed has decided that they will not start tightening monetary policy until unemployment hits 6.5% and/or inflation between 1 and 2 years ahead is projected to be no more than one half percentage point above the committee’s 2% threshold and longer term inflation figures continue to be well anchored. The good news is that this shift in policy now allows the markets to make their own projections about when these thresholds will be reached and can adjust their trading and investment strategies accordingly.

The Fed’s Monetary Policy and How it Can Impact Mortgage Rates

Fed Chairman Bernanke announced that the Fed will continue their threshold to spend $40 billion per month targeting Mortgage Backed Securities, reiterating the early message that improvement in the housing market through a low-rate environment will be most effective path to improve the economy. The big change comes in the decision to start changing monetary policy (heavily through interest rates) once inflation is projected to be 2.5% or higher over the next 1 or 2 years. Since inflation has a direct relationship with mortgage interest rates, it’s highly probable that once projected inflation reaches/exceeds those levels, interest rates will go up. The Fed will do all in its power to keep inflation with a target range. How does the Fed control inflation? They increase interest rates that they allow Banks to borrow money, which increases the rates that Banks have to charge to their clients.

Ahem… (raises hand). Is it possible that all of the printing of money to be able to spend the $85 billion on mortgage and long term securities possible a risk for higher inflation and higher interest rates?

Fed’s likely response: We have yet to be able to determine the efficacy of the quantitative easement.

Down the rabbit hole we go. Let’s just go ahead and pretend that printing $1 trillion a year is a cause for higher inflation….just pretending though.

If the projected inflation triggers the Fed to change its monetary policy, the Fed would immediately start to increase interest rates as a way to combat inflationary pressures and reduce the supply of money in the market (make it cost more to borrow). The end result is that the interest rates for consumers start to go up until the Fed sees inflation readings get back into the target range of 1.8% – 2%. By that time, investors around the globe are starting say, “Wait a minute, you’ve sold me these securities on long-term mortgage and other things and they’re paying me a rate of return of 1.5%-2% but based on projected inflation, my dollar is going to be losing 3% or more per year? So I’ll be losing money? No thanks, I’m out.”

So what happens, investors sell their long-term securities and the only way to entice them back into the market is to….that’s right, Raise the rate or yield that they are receiving on that security. In other words, we have to raise mortgage rates to a level that still gives investors a way to outpace inflation and make money.

The days of a 30 year fixed rate in the 3% – 4% range could be long gone, trending back to a level of normalcy of who knows, 6% or 7%? Only time will tell. Food for thought – if interest rates go up by one percent, a buyer looking in the $250,000 price range will have lost $30,000 in purchasing power. If interest rates go up to 6% (last seen less than 5 years ago), the same budget would only allow a $175,000 loan amount. That’s a difference of $75,000 in purchasing power. It’s time to start thinking seriously about your home buying and/or home selling strategy.

Our Strategy for Home Loan Interest Rates Going Forward

Home loan rates continue to trade near historic lows and should continue to stay in its trading range for the coming weeks and possibly months. At the same time, we do not see any reason that interest rates should get much lower than they are now, so if you are waiting around for a 2% rate on a 30 yr, we wish you the best of luck. If it were me, I would take advantage of interest rates sooner rather than later. While the Fed maintains its goal of keeping home loan rates low for the foreseeable future, the Fed cannot control the entire market. The $40 billion a month being used to target mortgage backed securities can help support the market, but overall market direction is based on many bigger picture items (ie. inflation, strength of global economy, Credit ratings, etc.).

Historically, interest rates tend to be lower in the winter and creep higher during the peak home buying season in the spring and through summer. We expect this trend to continue but will remain proactive with our clients and their home loan strategy. If you’re happy with your home loan options, take them while you can. Whether in 2013 or 2014, we are potentially only one bad inflation reading away from higher interest rates.

We maintain an ongoing dialogue with our clients about the market and interest rates throughout their financing experience so we can take advantage of the lowest rates when they present themselves. We all want the lowest rate, and the best way to ensure that you get the lowest rate, is to build a relationship with your mortgage planner, so they can best advise you on when to lock in your rate. Call us today for a complimentary mortgage review or Apply Online.

Mortgage Rate and Real Estate Update – Week of 12/03/12

No deal yet on the Fiscal Cliff and we know you’re getting tired of hearing about it. However, home ownership is a big part of the plan. Find out if home mortgage deductions are going away and how other news from the Fiscal Cliff talks will likely drive home loan interest rates for the coming weeks.

- Real Estate Investors – The $9.2 Billion Impact of 28.1 million U.S. Real Estate Investors

- How Fannie, Freddie, and Congress will use Home Mortgages to Fund Expanded Visa Program?

- Next Generation Buyers: Gen X and Gen Y Home Buyers are Savvy, Sophisticated and Ready to Buy

Mortgage interest rate and real estate news from last week:

Talks of the fiscal cliff issues continue to dominate the newswires and the mindsets of traders. The past week has seen mortgage backed securities hold strong near historic lows and above the 50 day moving average. The volatility picked up last Tuesday as progress was reported surrounding the fiscal cliff issues. The positive rumored news immediately helped Stocks rally over 200 points, taking the wind out of the sails of mortgage backed securities. This was just a glimpse of how big of an impact the fiscal cliff news will be going forward. The good news for home loan rates came when they were able to hold on to support at the 50 day-moving-average, proving this level to be a very strong floor of support and a benchmark worse-case scenario for the near-term.

What’s coming up this week on the economic calendar and what’s the impact on interest rates?

All eyes and ears will continue to be on news coming from the Fiscal Cliff talks. It’s all a matter of raising revenues and reducing costs, unfortunately for homeowners and prospective home buyers, eliminating the mortgage interest tax deduction would be a major source of tax revenue. If any changes are made to the tax deductions of mortgage interest, they are likely to be phased out over many years.

With the fiscal cliff talks ongoing, the economic calendar is full of employment and jobs data. Starting on Wednesday with the release of the ADP National Employment Report and rounding out with the Jobs Report on Friday, there is little ‘good’ news expected. Given the impact of storms on the East coast, there will likely be an increase in the Unemployment Rate and Initial jobless claims.

Here’s our strategy for the days and weeks ahead…

As home loan rates hover near historic lows and above support at the 25 and 50 day moving average, home loan rates are not expected to make a large move in either direction. As trading slows into the holiday season, any volatility that would drive home loan rates is likely to come from the fiscal cliff talks. We will recommend to cautiously float interest rates in the near term. However, should Congress find a resolution and back away from the cliff, expect the volatility to resurface at the possible expense of an increase in mortgage rates.

We maintain an ongoing dialogue with our clients about the market and interest rates throughout their financing experience so we can take advantage of the lowest rates when they present themselves. We all want the lowest rate, and the best way to ensure that you get the lowest rate, is to build a relationship with your mortgage planner, so they can best advise you on when to lock in your rate. Call us today for a complimentary mortgage review or Apply Online.

Mortgage Rate and Real Estate Update – Week of 11/26/12

It’s not a cyber Monday sale, home loan rates have actually been this low for a while now. Thanks to the fiscal cliff issues and Eurozone drama being front and center, interest rates are holding strong near historic lows.

Mortgage interest rate and real estate news from last week:

- Low mortgage rates allow buyers to afford up to 20% more in home price compared to 3 years ago

- The Fall and Rise of Jumbos – Homes values with jumbo mortgages fell hard, now rising Fast

- “G-Fees” drive up loan costs across the board for some states – Texas lucky to avoid this round, for now…

- Holiday tidbit – Wanting your own ’12 Days of Christmas’? The cost this year tops $107k

In a holiday shortened trading week, home loan interest rates and mortgage bonds were mostly unchanged. News that Europe is now in the midst of its second recession in four years and the U.S. weekly jobless claims coming it at their highest level in 18 months would typically spark more volatility, but interest rates seem to be comfortable in the current trading range established over the last month near historic lows. The low volume trading and friendly Bond news allows the Fed to keep their QE3 stimulus funds available for any major volatility that may come to the markets.

What’s coming up this week on the economic calendar and what’s the impact on interest rates?

With no major economic reports due for release this week, most attention will be placed on talks of a lawmakers reaching a resolution on the fiscal cliff issues. The markets will also be closely watching a meeting of finance ministers in the Eurozone as they digest news of the recession. The battle grows deeper as major Euro countries like Germany, refuse to participate in further “bail-outs” of Greece unless they can make further budget cuts and commit to repay some of their debt.

In the midst of the global economic soap opera, the Treasury will be auctioning off $99 Billion in Notes this week. Depending on the investor appetite of the 2, 5, and 7 year Note auctions, we could see volatility creep back into the Bond markets. On the flip side, should the auction go well, the S&P 500 could slip further from its 200 day moving average, allowing home loan rates to move closer to all time lows.

Here’s our strategy for the days and weeks ahead…

Interest rates for home loans have found a comfortable trading range over the last 30 days and have managed to create a solid level of support just beneath current levels. As long as mortgage Bonds can manage to remain above this key technical support, interest rates have a great chance to rally and move closer to all time lows for interest rates. Our advice would be to float in the near term unless something changes, causing pricing to break through support. With the amazingly low interest rates available to homeowners and home buyers, the time is now to consider their options for a refinance or start their planning for a home purchase.

We maintain an ongoing dialogue with our clients about the market and interest rates throughout their financing experience so we can take advantage of the lowest rates when they present themselves. We all want the lowest rate, and the best way to ensure that you get the lowest rate, is to build a relationship with your mortgage planner, so they can best advise you on when to lock in your rate. Call us today for a complimentary mortgage review or Apply Online.